BNPL: The Gen Z Take

Buy-now-pay-later (BNPL) services have transformed the payments landscape, offering young consumers a new way to manage their purchases and budgets. Brands like Klarna, Clearpay, Scalapay, and Alma have gained popularity by providing short-term, often interest-free financing, enabling consumers to spread out payments over time.

However, this growth has not been without controversy. Regulators and consumer groups are increasingly concerned about BNPL’s potential to fuel overspending, particularly among younger or financially vulnerable individuals. Some media outlets have even labeled Gen Z the “debt-fueled” generation.

So, what do Gen Z themselves think about the topic?

Gen Z’s Strong Appetite for BNPL

Despite the concerns, Gen Z has shown a strong appetite for BNPL services. Nearly 1 in 5 (18%) of Gen Z consumers in France, Germany, and the Netherlands actively use BNPL, with an additional 17% expressing a strong intention to do so.

Users cite flexibility, convenience, and financial freedom as key benefits:

• “I can buy things when I need them” (36%)

• “I can choose payment plans that suit my needs” (29%)

• “I have more financial freedom” (28%)

They are using BNPL in two main scenarios: purchasing big-ticket items that are unaffordable upfront (37% of Gen Z overall, and more common among Males 44%) and trying out products or services before fully committing to them (38%, and more commonly among Females 43%).

Awareness of the pitfalls

Gen Z is not blind to the potential risks of BNPL. While they embrace the advantages, they also voice concern about the potential for BNPL to encourage impulsive spending and lead to debt. Nearly half (47%) of Gen Z BNPL users say that the services “encourage me to spend when I know I shouldn’t” and nearly 1 in 3 (32%) say they feel unfairly targeted.

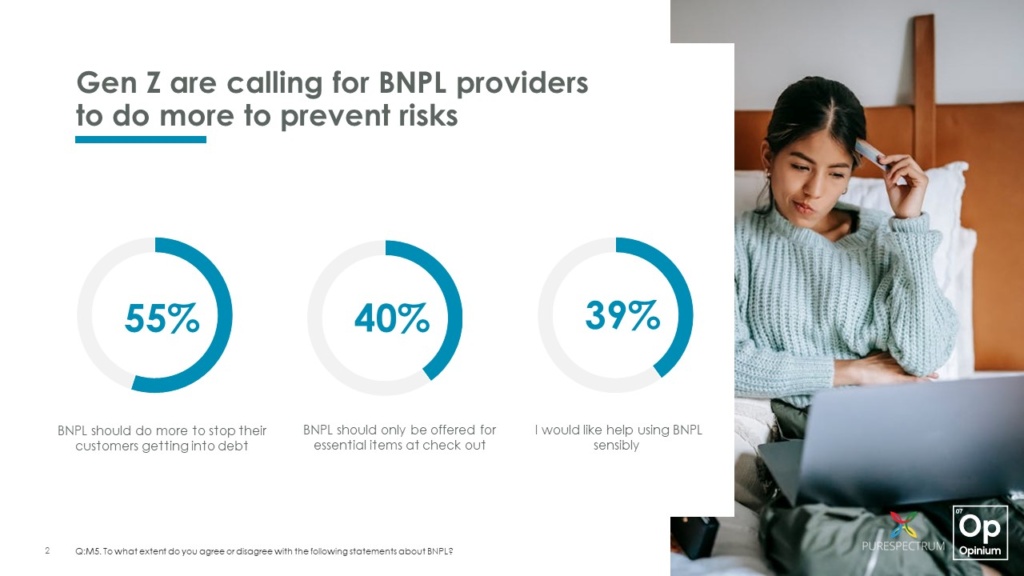

Gen Z are calling for BNPL providers to do more

On a personal level, Gen Z want BNPL providers to offer them more guidance and support, with nearly half (45%) of users expressing a desire for help using BNPL sensibly.

They also recognize a need for more responsible practices within the industry. 65% of users and 55% of Gen Z overall believe BNPL companies should take greater measures to prevent customers from falling into debt.

Despite the high levels of usage for big-ticket items, 40% of Gen Z agree that BNPL should only be offered for essential items at checkout. This reflects an awareness among young consumers about the potential risks of BNPL and desire for greater protection against overspending for themselves and their peers.

Balancing Innovation with Responsibility

The rise of BNPL services reflects a broader trend of financial democratization, empowering young consumers with greater flexibility and control over their purchases. However, Gen Z want this innovation by service providers to come with responsibility to protect them from potential harm.

If you’d like to find out more about the research or arrange a call with one of the team to take you through the findings of our research into Gen Z in more detail please email europe@opinium.com.

‘Opinium surveyed 3,000 people within the Netherlands, France and Germany, aged 16 to 27 years old, during February 2024’.